Corporate Engagements

As expressed in our Investment Beliefs, we believe long-term value creation requires effective management of three forms of capital: financial, physical, and human. Our corporate engagement activities are supported by this belief and are conducted privately and confidentially with our portfolio companies.

We engage our portfolio companies to encourage them to consider how environmental, social, and governance (ESG) risks and opportunities affect their ability to create value over the long-term.

We will generally engage with portfolio companies under three broad categories:

- Ad hoc Engagements: these are generally triggered by specific events and are centered around controversies or governance concerns.

- Routine Engagements: these involve calls with our portfolio companies during the proxy voting off season and prior to casting our vote at annual general meetings (AGMs). Routine engagements do not overlap with ad hoc or initiative-based engagements.

- Initiative-based Engagements: these are related to CalPERS' strategic and core initiatives outlined in the Total Fund Governance & Sustainability 5-Year Strategic Plan (PDF).

Process

We exercise our ownership rights to influence how our portfolio companies are managed and governed. Our underlying objective is to ensure that our portfolio companies are managed to create long-term, sustainable value for shareowners. Our engagement process involves clear communication with companies regarding our engagement objectives and is meant to be collaborative.

Identify

We identify company concerns directly or through our stakeholders. We use the following prioritization framework, outlined in our Investment Beliefs, in considering whether to engage on issues raised by stakeholders:

- Principles and Policy - to what extent is the issue supported by CalPERS Investment Beliefs, Governance & Sustainability Principles or other Investment Policy?

- Materiality - does the issue have the potential for an impact on portfolio risk or return?

- Definition and Likelihood of Success - is success likely, in that CalPERS' action will influence an outcome which can be measured? Can we partner with others to achieve success or would someone else be more suited to carry the issue?

- Capacity - does CalPERS have the expertise, resources, and standing to influence an outcome?

Analyze

Our corporate governance team will perform a preliminary analysis of the issues before engaging with a portfolio company. We will review each company's public documents, which may include its annual report, integrated report, Securities and Exchange Commission (SEC) filings, sustainability reports, and any other publicly available information. We will also use ESG research provided by third-party vendors to complement our analysis.

After conducting a thorough review and analysis of the company and issue, we will determine whether a corporate engagement is still warranted based on our Investment Beliefs and Governance & Sustainability Principles. If so, we will proceed to request an engagement with the company.

Engage

We engage our portfolio companies confidentially through phone, letter, and/or in-person meetings. We have the following objectives as we engage portfolio companies:

- To gather facts about the issue(s) and express our concerns to the company

- To share CalPERS' Governance & Sustainability Principles and Investment Beliefs with the company

- To seek the company's perspective on the issue

- To seek a resolution to address our concerns related to the issue

Resolve

We will periodically review the company's progress towards a resolution to determine our next course of action.

- Positive Resolution: The company responds to our engagements and participates in an active constructive dialogue with us. In such instances, we will continue to monitor these companies to ensure they implement any commitments made.

- No Resolution: If we determine our engagement efforts have not been successful, we will exercise our shareowner rights consistent with our Governance & Sustainability Principles, which may include the following actions:

- Oppose ballot items raised at the company's annual general meeting

- File shareowner proposals at the company

- Implement a shareowner engagement campaign

- Collaborate with partners

- Make a public statement of dissatisfaction

Initiatives

Empirical evidence shows companies with diverse boards and executives tend to have better financial performance than less diverse companies. Better financial performance leads to better investment returns, which improves our ability to pay benefits.

More than half of every dollar we pay out in benefits comes from our investment returns. Improving corporate board diversity can enhance our investment returns.

Objective

In August 2016, our Board's Investment Committee adopted the Total Fund Governance & Sustainability 5-Year Strategic Plan (PDF) which identified improving corporate board diversity & inclusion as one of six strategic priorities of the Investment Office. The objective of this initiative is to improve corporate board diversity to enhance our total fund performance.

Consistent with our Governance & Sustainability Principles (PDF), we believe a company's board should reflect a diverse mix of skills, characteristics, backgrounds, and experiences. Our long-term goal is to ensure that all public companies we invest in have a level of board diversity that reflects each company's business, customer base, workforce, and society in general.

Process

We use third-party data to annually identify companies in our portfolio that lack elements of board diversity. We write letters to the board chair of each company requesting information on how diversity is considered in the context of board composition, refreshment, and nomination. Additionally, we request each company to develop and publicly disclose its diversity policy and implementation plan for improving board diversity.

In instances where the companies do not respond to our initial letter, we make multiple attempts to engage before escalating the issue by filing shareowner proposals at those companies. While we prefer to work in partnership with our portfolio companies, by engaging privately and confidentially, we will use proxy voting and shareowner campaigns as tools to bring change where engagements have not led to constructive outcomes.

Proxy Voting Strategy

Based on the company's level of responsiveness to our efforts to engage on board diversity, we will consider the following actions:

- No Response: We will withhold votes from the board chair, nominating/governance committee members, and long-tenured directors.

- Inadequate Response: We will withhold votes from the nominating/governance committee members and long-tenured directors.

- Adequate response: We will monitor the company to ensure that it implements its committed actions.

- Shareowner proposals: We will vote in support of shareowner proposals related to diversity that are consistent with our Governance & Sustainability Principles.

Shareowner Campaigns

Additionally, we will consider the following activities:

- We will file majority vote for director elections shareowner proposals at nonresponsive companies that do not have majority voting for director elections.

- We will run proxy solicitations on shareowner proposals related to corporate board diversity at portfolio companies as appropriate.

Outcomes

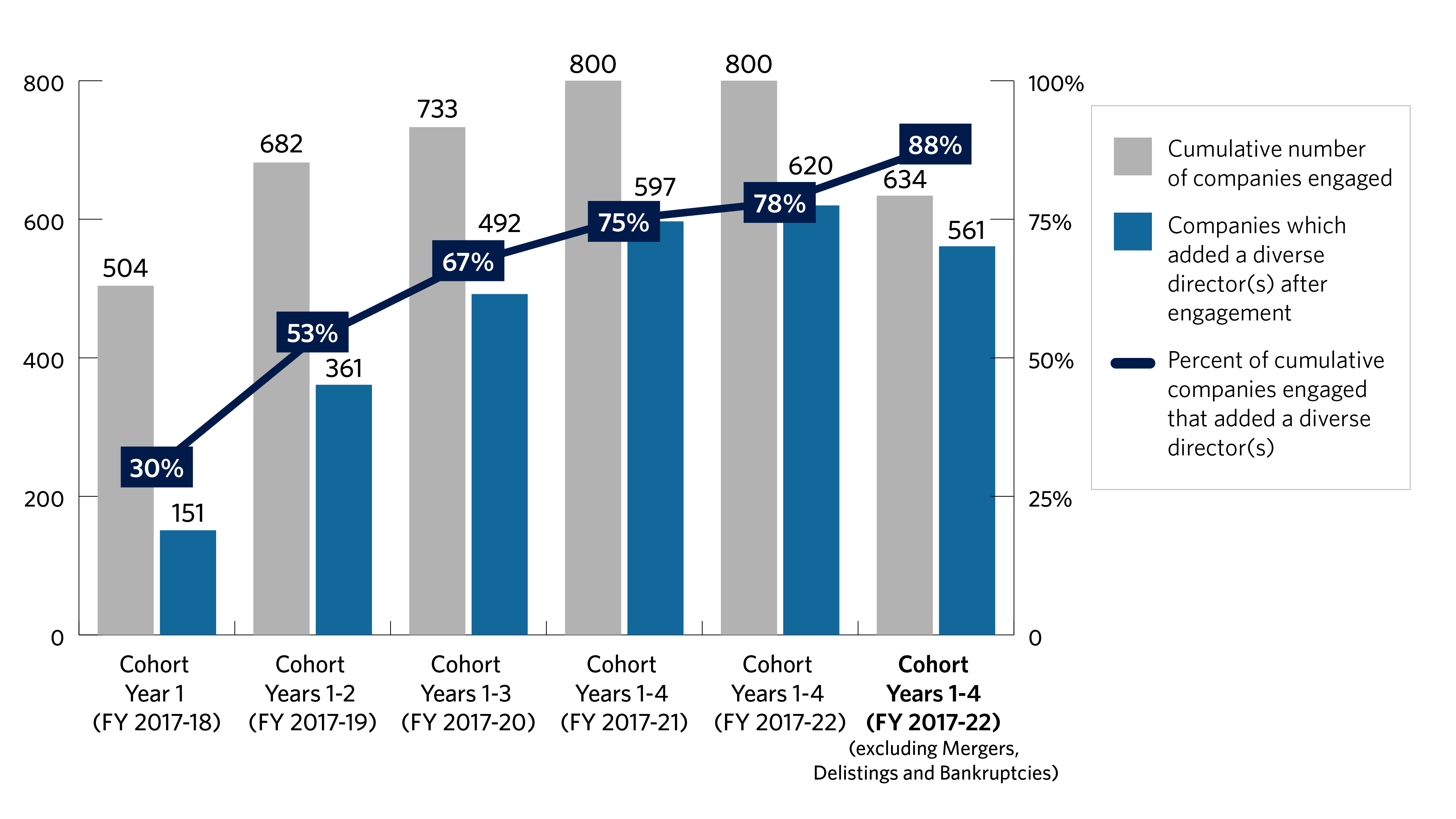

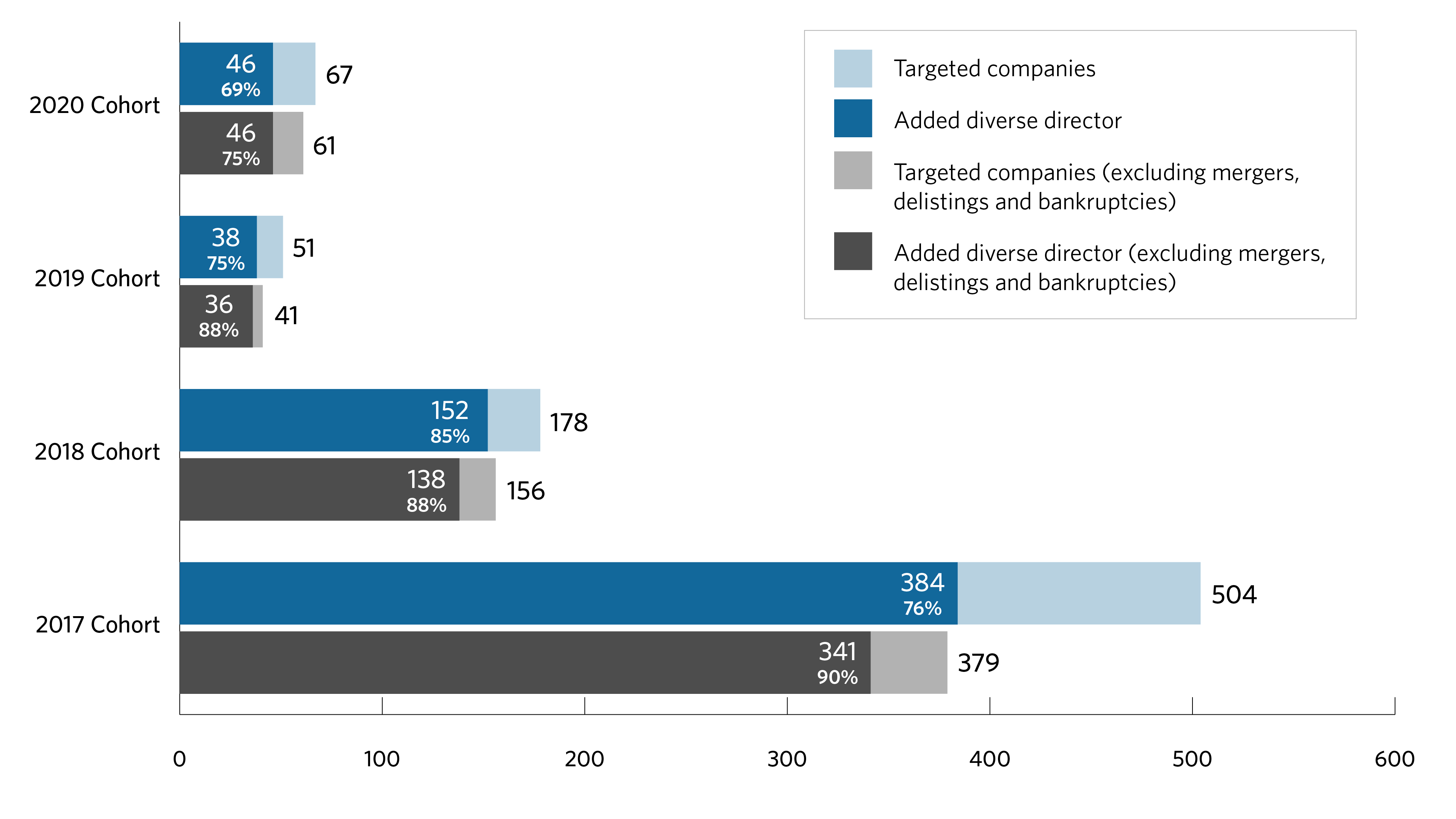

- Since fiscal year 2017-18, we've engaged 800 companies in the Russell 3000 index requesting they improve diversity on their boards (Figure 1). Of the 800 companies engaged, 620 companies (approximately 78%) have since added elements of board diversity that they did not have prior to our engagement. Figure 2 shows the board diversity engagement targets by cohort year, and also those excluding mergers, delistings and bankruptcies.

- During the 2018 to 2022 proxy seasons, we voted against over 1,100 directors in aggregate where our engagement efforts did not result in constructive outcomes.

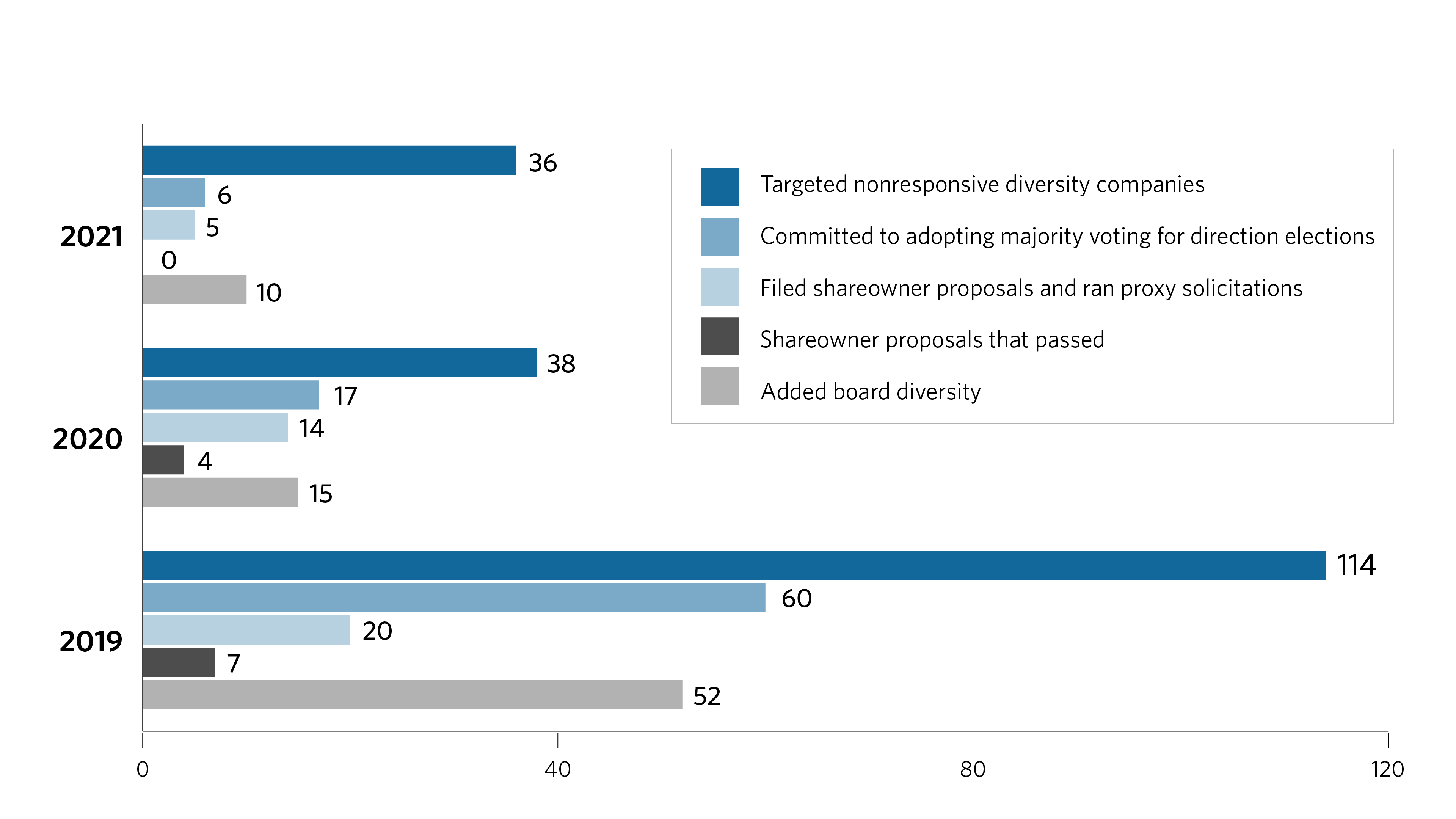

- During the 2021 proxy season, we targeted 36 nonresponsive diversity companies seeking the adoption of majority vote for director elections (Figure 3). We had successful engagements at 6 companies that committed to the adoption of majority vote for director elections. We filed shareowner proposals and ran proxy solicitations at 5 companies, none of which had received a majority shareowner support. Ten of the 36 target companies have added elements of board diversity that they did not have prior to our engagement.

- During the 2020 proxy season, we targeted 24 nonresponsive diversity companies for “vote no” campaigns. We had successful engagements at 12 companies that added elements of board diversity that they did not have prior to our engagement. We ran public “vote no” campaigns at nine companies where we could not reach a settlement. These campaigns included proxy solicitations urging shareholders to vote “against” board chairs, nominating/governance committee members, and long-tenured directors. One target company delisted while the remaining two companies continue to be ongoing engagements.

- During the 2021 proxy season, we targeted 20 nonresponsive diversity companies for “vote no” campaigns. We had successful engagements at 6 companies that added elements of board diversity that they did not have prior to our engagement. We ran public “vote no” campaigns at 3 companies where we could not reach a settlement. These campaigns included proxy solicitations urging shareholders to vote “against” board chairs, nominating/governance committee members, and long-tenured directors. One target company delisted while the remaining two companies continue to be ongoing engagements.

Climate change presents systemic physical and transition risk to CalPERS' investments. This can affect investment returns.

Background

In 2015, we conducted a carbon footprint evaluation of the 10,000+ public companies within our portfolio. We found that the emissions were heavily concentrated - about 80 companies were responsible for over 50% of the portfolio's greenhouse gas emissions. In 2017, we worked with global organizations and fellow investors to establish the Climate Action 100+ (CA100+) initiative. The CA100+ is included in our Total Fund Governance & Sustainability Strategic Plan (PDF). We served as the inaugural Chair of both the Climate Action 100+ Steering Committee until 2019. Currently, we're a member of the Steering Committee and of the Asia Advisory Group.

The CA100+ is a five-year initiative led by investors to engage systemically important greenhouse gas emitters and other companies across the global economy that have significant opportunities to drive the clean energy transition and help achieve the goals of the Paris Agreement. Signatories to the CA100+ include 600+ investors with over $55 trillion (USD) in assets under management.

Objective

As part of the CA100+ initiative, the Corporate Governance team leads the engagement of 22 portfolio companies to ensure their strategies consider the risk and opportunities arising from climate change. Specifically, the team engages portfolio companies requesting their boards and senior management to do the following:

- Implement a strong governance framework which clearly articulates the board's accountability and oversight of climate change risks and opportunities.

- Take action to reduce greenhouse gas emissions across their value chain, consistent with the Paris Agreement's goal of limiting global average temperatures increase to well below 2-degrees Celsius above pre-industrial level.

- Provide enhanced corporate disclosure in line with the final recommendations of the Task Force on Climate-related Financial Disclosure (TCFD) and, when applicable, sector-specific Global Investor Coalition on Climate Change Investor Expectations on Climate Change to enable investors to assess companies' business plans against a range of climate scenarios, including well below 2-degree Celsius, and improve investment decision-making.

Proxy Voting Strategy

- We support shareowner proposals aligned with our Governance & Sustainability Principles (PDF) such as those that request for accurate and timely disclosure surrounding environmental risks and opportunities associated with climate change risk.

- In 2022, we implemented an enhanced voting practice by considering specific climate-related criteria to help inform director votes at all CA100+ companies. This is a new voting practice to hold directors accountable on climate change just as we do with diversity and executive compensation.

- 2022 Proxy Season: We voted “against” 95 directors at 26 CA100+ portfolio companies.

Shareowner Campaigns

- If necessary, we will file or co-file climate shareowner proposals at portfolio companies.

- In 2015 and 2016, we co-filed on shareowner proposals led by the Aiming for A coalition of asset owners. The Aiming for A proposals were filed at multiple European energy and mining companies requesting improved disclosure of the risks and opportunities posed by climate change.

- In 2017, we co-filed climate risk shareowner proposals at three U.S. oil and gas companies. For the first time, an environmental-related shareowner proposal filed at a U.S. company achieved majority shareowner support. We also ran public proxy solicitations at 13 U.S. companies in support of improved climate risk reporting.

- In 2018, we ran public proxy solicitations at five U.S. companies in support of improved climate-risk reporting. Note, fewer proposals went to vote in 2018 (compared to 2017) due to implementation by companies.

- In 2019, we filed and co-filed climate risk shareowner proposals at four Climate Action 100+ companies.

- In 2020, we co-filed on one climate-related shareowner proposal and ran proxy solicitations for climate-related proposals at 10 portfolio companies that were flagged by the Climate Action 100+.

- In 2021, we filed and co-filed climate-related shareowner proposals at three CA100+ companies and ran proxy solicitations for climate-related proposals at six portfolio companies that were flagged by the CA100+.

- In 2022, we filed and co-filed climate related shareowner proposals at two CA100+ companies and ran proxy solicitation for climate-related proposal at one portfolio company that was flagged by the CA100+.

Outcomes

- We've initiated engagements with all 22 portfolio companies.

- In general, companies are responding favorably by improving the governance of climate-related risks, curbing GHG emissions, and strengthening climate-related financial disclosures.

- Results and progress of collaborative engagements are detailed in the Climate Action 100+ 2020 Progress Report.

In 2019, we launched a new Executive Compensation Analysis Framework (PDF) for evaluating executive compensation plans at our portfolio companies. View our Executive Compensation Analysis Framework: Frequently Asked Questions (PDF) for answers to commonly asked questions from our engagements on executive compensation with directors and management of our portfolio companies.

Process

We use our Executive Compensation Analysis Framework to evaluate advisory vote on executive compensation proposals at our portfolio companies. When we vote against the advisory vote on executive compensation proposal, we write letters to the compensation committee chair of each company requesting a meeting to discuss our concerns.

Proxy Voting Strategy

In 2020, we began withholding votes from directors who are compensation committee members in the same year that we voted against the advisory vote on executive compensation.

Outcomes

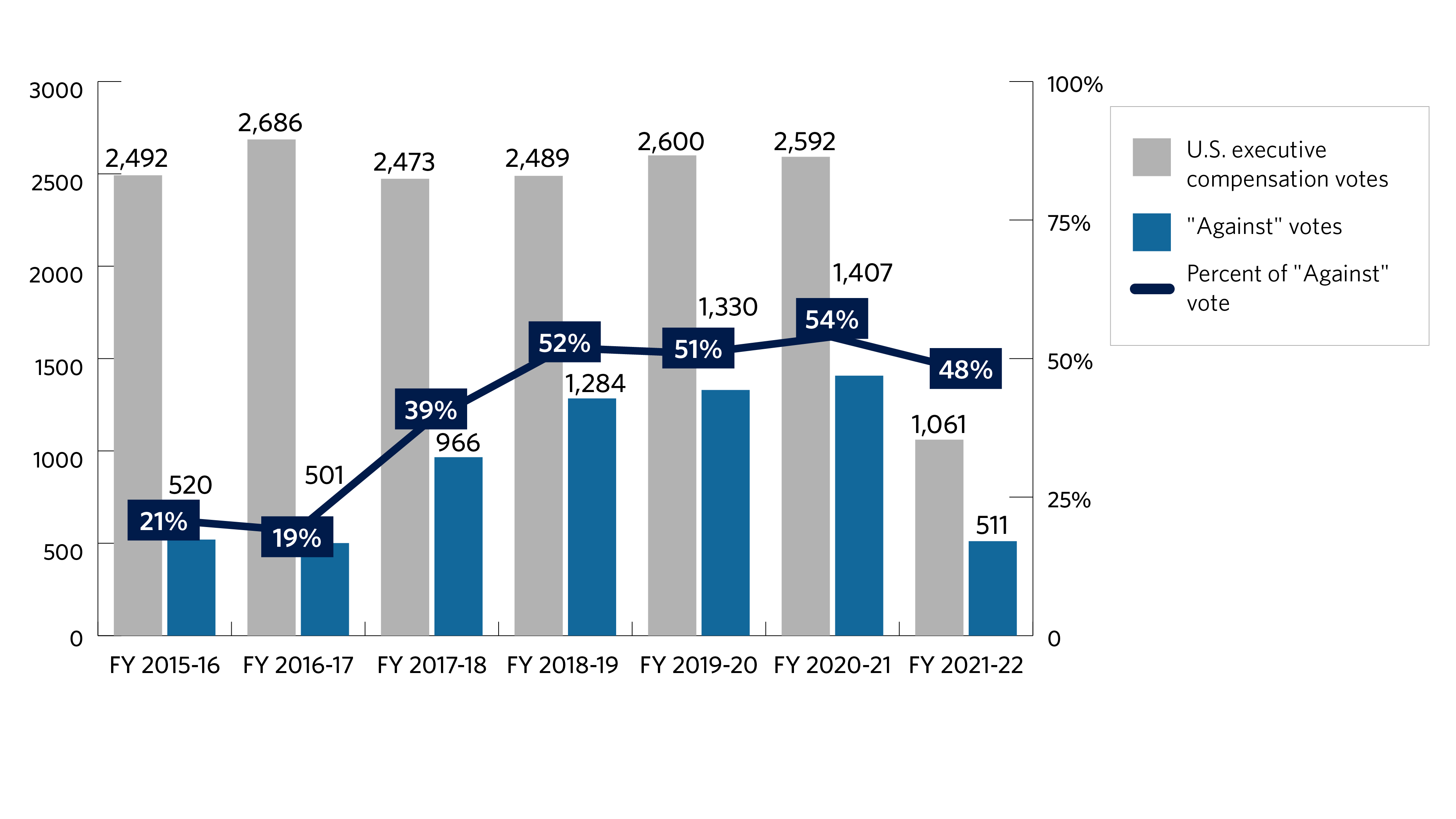

During fiscal year 2021-22, we voted against 48% of advisory vote on executive compensation proposals. Additionally, we voted against over 1,342 directors when voting against the advisory vote on executive compensation.

Japan is our second largest investment market in our global equity portfolio. U.S. research shows Japanese companies have historically lagged their global peers on profitability, valuation, and board independence. Consistent with our Governance & Sustainability Principles, we believe that independent, competent, and diverse boards are the foundation to a sound governance structure and could help improve investment returns of Japanese companies. We believe strong governance practices increase the likelihood that companies will perform better over the long-term.

Background

Our work to advance corporate governance best practices in Japan dates back more than a decade. In 2014, we collaborated with a group of international institutional investors and wrote to many of our largest Japanese portfolio companies requesting that the board of directors be comprised of at least one-third independent directors by 2017. Subsequently, in 2015, we publicly supported the adoption of Japan's Corporate Governance Code and were one of the first U.S. signatories to disclose our commitment (PDF) to Japan's Stewardship Code in 2016. Japan's Stewardship Code aims to enhance long-term returns for investors through constructive engagement and dialogue with publicly traded Japanese companies. In April 2018, we submitted comment to the Tokyo Stock Exchange (TSE) on the proposed revisions to Japan's Corporate Governance Code, reinforcing our belief that a one-third independence level for the board of directors in Japan should be the minimum acceptable threshold at this time.

Objective

Our goal is to improve board independence at Japanese portfolio companies by moving the market towards majority independent boards consistent with our Governance & Sustainability Principles (PDF).

Proxy Voting Strategy

- In 2017, we implemented an enhanced voting practice for Japan to vote "against" non-independent directors when board independence is less than one-third. We communicated the change in our voting practice to the Japan Financial Services Agency and publicized it through the local Japanese media.

- 2017 Proxy Season: We voted "against" 6,509 non-independent directors at 864 of approximately 1,200 companies and wrote letters to communicate voting rationale and encourage the appointment of independent directors to reach at least 1/3 independence threshold.

- 2018 Proxy Season: We voted "against" 6,124 non-independent directors at 794 of approximately 1,200 companies and wrote letters to communicate voting rationale and encourage the appointment of independent directors to reach at least 1/3 independence threshold.

- 2019 Proxy Season: We voted "against" 5,225 non-independent directors at 682 of approximately 1,200 companies due to less than 1/3 board independence.

- 2020 Proxy Season: We voted “against” 3,712 non-independent directors at 504 of approximately 1,273 companies due to less than 1/3 board independence.

- 2021 Proxy Season: We voted “against” 2,928 non-independent directors at 395 companies of approximately 1,392 companies due to less than 1/3 board independence.

- 2022 Proxy Season: We voted “against” 936 non-independent directors at 126 companies of approximately 861 companies due to less than 1/3 board independence.

Outcomes

- We are grateful to the local market constituents for their hard work and leadership that has been put into the corporate governance reforms in Japan. We continue to support their ongoing efforts.

- Independence levels for the 864 companies that we wrote letters to in 2017 requesting that they consider increasing the level of board independence to at least 1/3 have improved on par with the trend of the broader Japanese market.

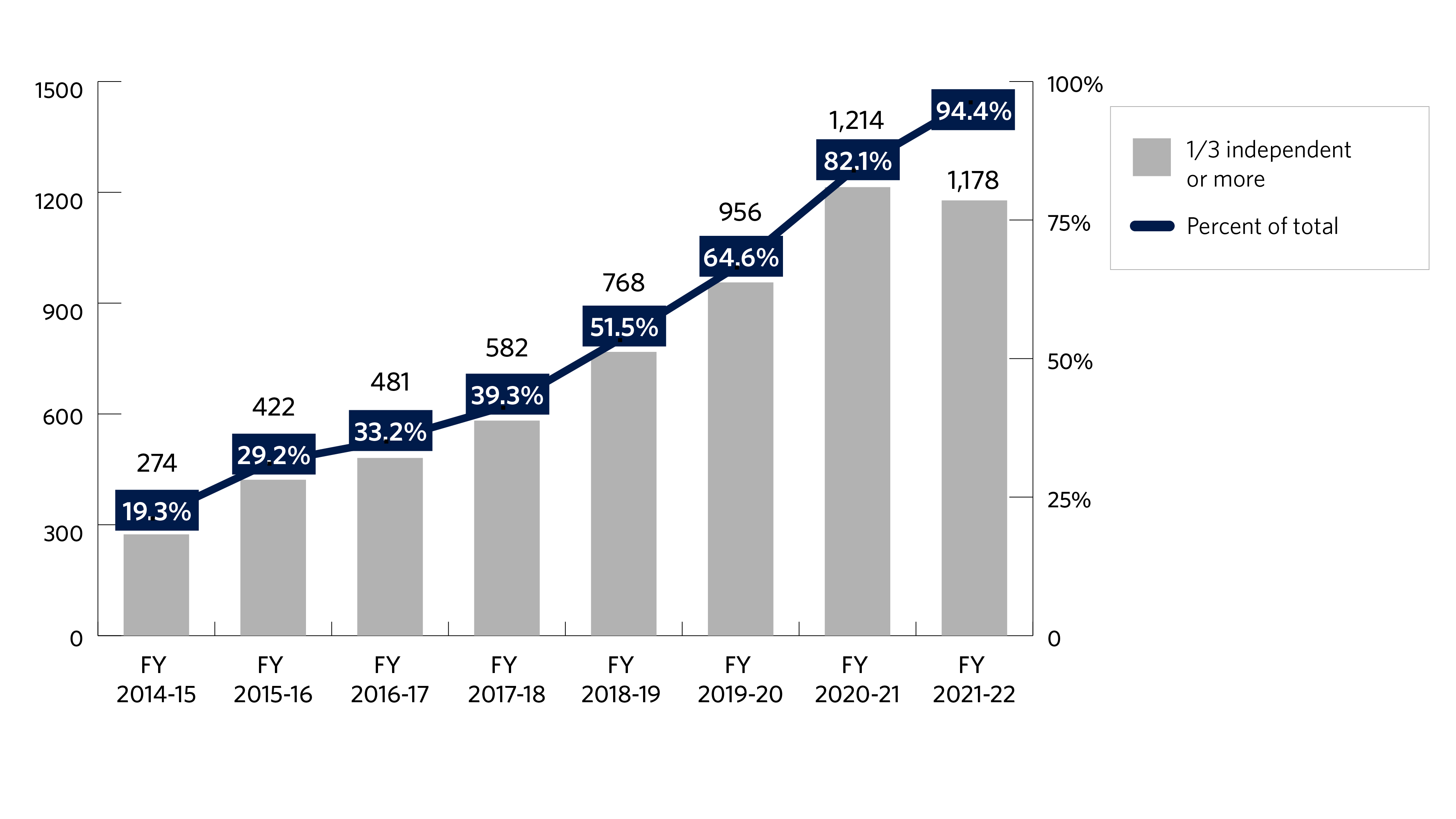

- The percentage of Japanese companies with one-third board independence rose 19% in 2015 to about 94% in 2022 (Figure 1).

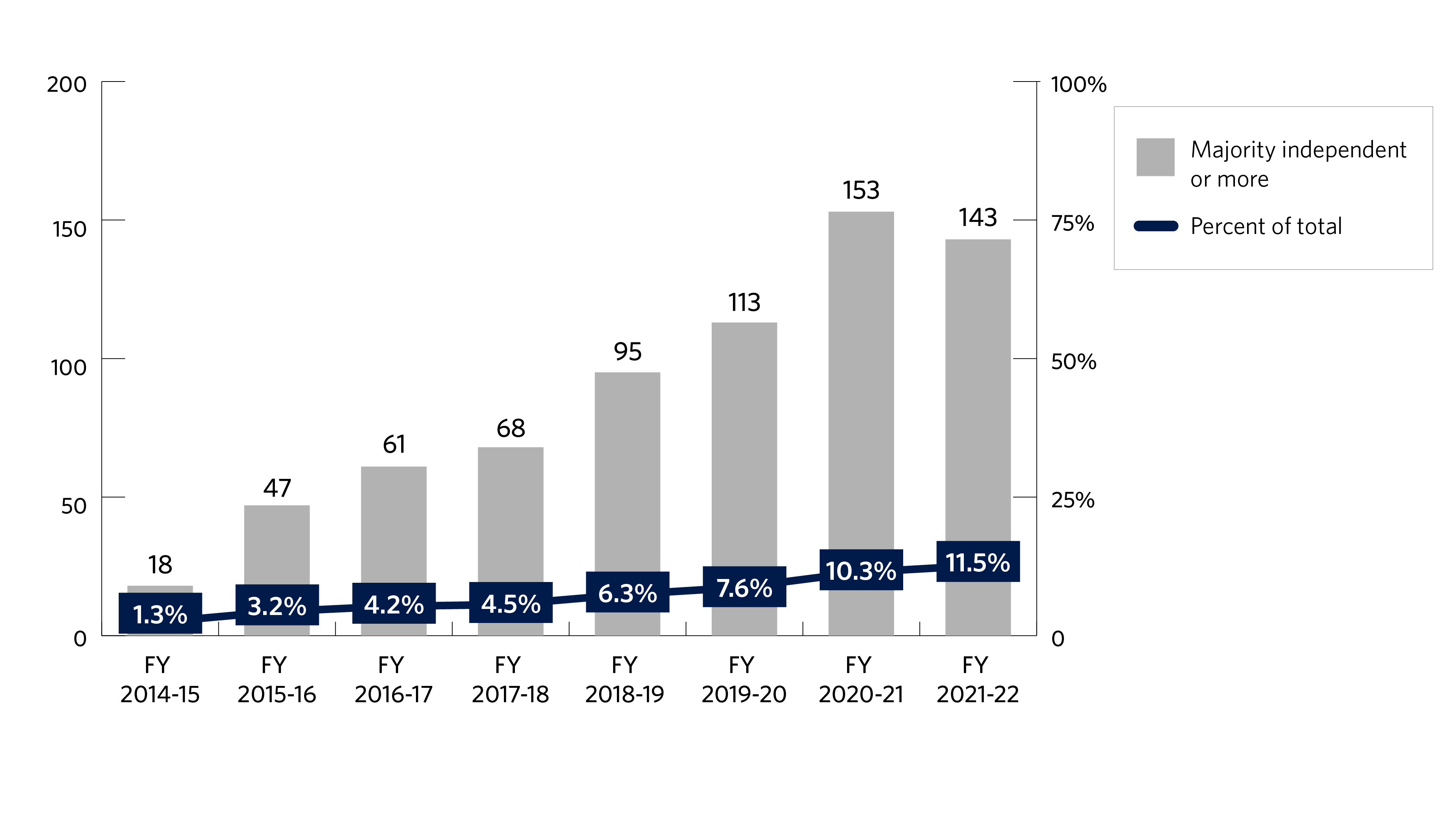

- The percentage of Japanese companies with majority independent boards increased from 1% in 2015 to about 11% in 2022 (Figure 2).

Many companies retain a plurality voting system to elect directors to the board. Under plurality voting, a director with the highest number of votes gets elected to the board. If a director runs unopposed, plurality voting allows the director to be elected with a single "for" vote, regardless of the number of "withhold" or "against" votes.

Directors elected by plurality voting do not need a majority of the votes cast. To reform the director election process, we engage portfolio companies to request adoption of a majority vote standard for director elections. Companies that adopt a majority voting standard for director elections would require a director to receive a majority of votes cast to be elected to the board, while those receiving less than the majority of the votes cast are required to tender their resignation to the board within 90 days after the voting results are determined.

Objective

Our goal is for companies to reform their director election process by replacing a plurality voting standard with a majority vote standard for director elections. This will ensure that directors are accountable to shareowners.

Process

From 2010 to 2018, we engaged 50 companies each year to request adoption of a majority voting standard for director elections. In 2019, we transitioned our majority vote engagements from being a standalone initiative to being part of our corporate board diversity & inclusion initiative. Of the companies that do not respond to our diversity engagement letters, we identify the ones with a plurality voting system and write letters requesting adoption of majority voting for director elections. In situations where our engagements do not lead to constructive outcomes, we write to the companies informing them of our intention to file shareowner proposals seeking adoption of majority voting for director elections.

Proxy Voting Strategy

- We will vote in support of shareowner proposals requesting adoption of majority voting for director elections.

Shareowner Campaigns

- We will file shareowner proposals on majority voting for director elections at companies that do not respond to our diversity engagement letters and do not also have majority voting for director elections.

- We will run proxy solicitations for our shareowner proposals on majority voting for director elections.

Outcomes

- Since 2010, 385 of the 400 companies (approximately 97%) we engaged under the standalone majority voting initiative, which ended in 2018, have either adopted or committed to adopt a majority vote standard for director elections.

- During the 2021 proxy season, we targeted 36 nonresponsive diversity companies seeking the adoption of majority vote for director elections (Table 1). We had successful engagements at 6 companies that committed to the adoption of majority vote for director elections. We filed shareowner proposals and ran proxy solicitations at 5 companies, none of which had received a majority shareowner support. Ten of the 36 target companies have added elements of board diversity that they did not have prior to our engagement.

| Proxy Season | Targeted Nonresponsive Diversity Companies | Committed to Adopting Majority Voting for Direction Elections | Filed Shareowner Proposals and Ran Proxy Solicitations | Shareowner Proposals That Passed | Added Board Diversity |

|---|---|---|---|---|---|

| 2019 | 114 | 60 | 20 | 7 | 52 |

| 2020 | 38 | 17 | 14 | 4 | 15 |

| 2021 | 36 | 6 | 5 | 0 | 10 |

Proxy access is a corporate governance provision giving shareowners the right to nominate director candidates to a company board for inclusion on proxy voting ballots. Specifically, we believe shareowners should have effective access to the director nomination process, also known as proxy access.

Companies should provide access to management proxy materials for a group of long-term investors owning in aggregate at least 3% of a company's voting stock to nominate up to 25% of the board. Eligible investors must have owned the stock for at least three years. As a useful resource regarding the specific best practices for the proxy access components, refer to the CII Proxy Access Best Practices.

Objective

Our goal is to have portfolio companies adopt proxy access bylaws, providing shareowners the ability to effectively nominate directors. The provision will help to ensure that corporate boards are independent, competent, diverse, and accountable to shareowners.

Process

In 2015, we identified proxy access as a priority and began engaging companies and regulators on the merits of the corporate governance best practice. Each year we formally target 25 or more companies and write each company a letter requesting to engage on the issue. In situations where our engagements do not lead to constructive outcomes, we write to companies informing them that we will be filing proxy access shareowner proposals.

Proxy Voting Strategy

- We will vote to support shareowner proposals on proxy access.

Shareowner Campaigns

- We engage portfolio companies to request the adoption of proxy access and file shareowner proposal in instances where settlements cannot be reached.

- We will run proxy solicitations related to our proposals on proxy access.

Outcomes

- From 2015 to 2018, individually and in partnership with other investors, we filed proposals, engaged companies, attended company annual general meetings, and ran proxy solicitations to gain support on proxy access at over 100 companies.

- In July 2019, we targeted 25 companies requesting the adoption of proxy access. We reached settlements with 25 companies that committed to adopt proxy access.

- In 2020, we targeted 25 companies requesting the adoption of proxy access. We reached settlements with 22 companies that committed to adopt proxy access.

- In 2021, we targeted 50 companies requesting the adoption of proxy access. We reached settlements with 38 companies that committed to adopt proxy access.

- In 2022, we targeted 50 companies requesting the adoption of proxy access. We reached settlements with 31 companies that committed to adopt proxy access.